Executive Summary

This document develops a design specification for a 30-year, Canada–Korea co-issued sovereign infrastructure bond financing a Fort McMurray–to–Prince Rupert heavy-oil pipeline corridor, with a derivative overlay (cross-currency, interest-rate, basis swaps), KPI-linked step-up/step-down coupons, an Indigenous co-ownership tranche embedded at issuance, and a programmatic execution layer drawing on existing tokenised-bond market infrastructure. The instrument is to be priced as a spread over US Treasuries — used as the universal benchmark, not as a target.

The strategic objective is counterparty risk diversification, not antagonism. Canada is the most open major economy in the world to a single counterparty (the United States, ~75% of merchandise exports), and the freezing of roughly half of the Bank of Russia's reserves in February 2022 confirmed that even friendly G7 jurisdictions can find themselves locked out of dollar and euro reserve assets when geopolitical alignments shift. A Central Banking / HSBC reserve managers' survey found 84.5% of central bank reserve managers believe weaponisation of reserves will have significant consequences for the future of reserve management. The instrument proposed here is designed to sit comfortably within that mainstream institutional reaction: an additional, AAA-quality, Pacific-anchored safe-asset substitute that placed money — Korean NPS / KIC / KP, Canadian Maple 8, EU pension funds, GCC SWFs — can buy without political controversy.

Key design conclusions

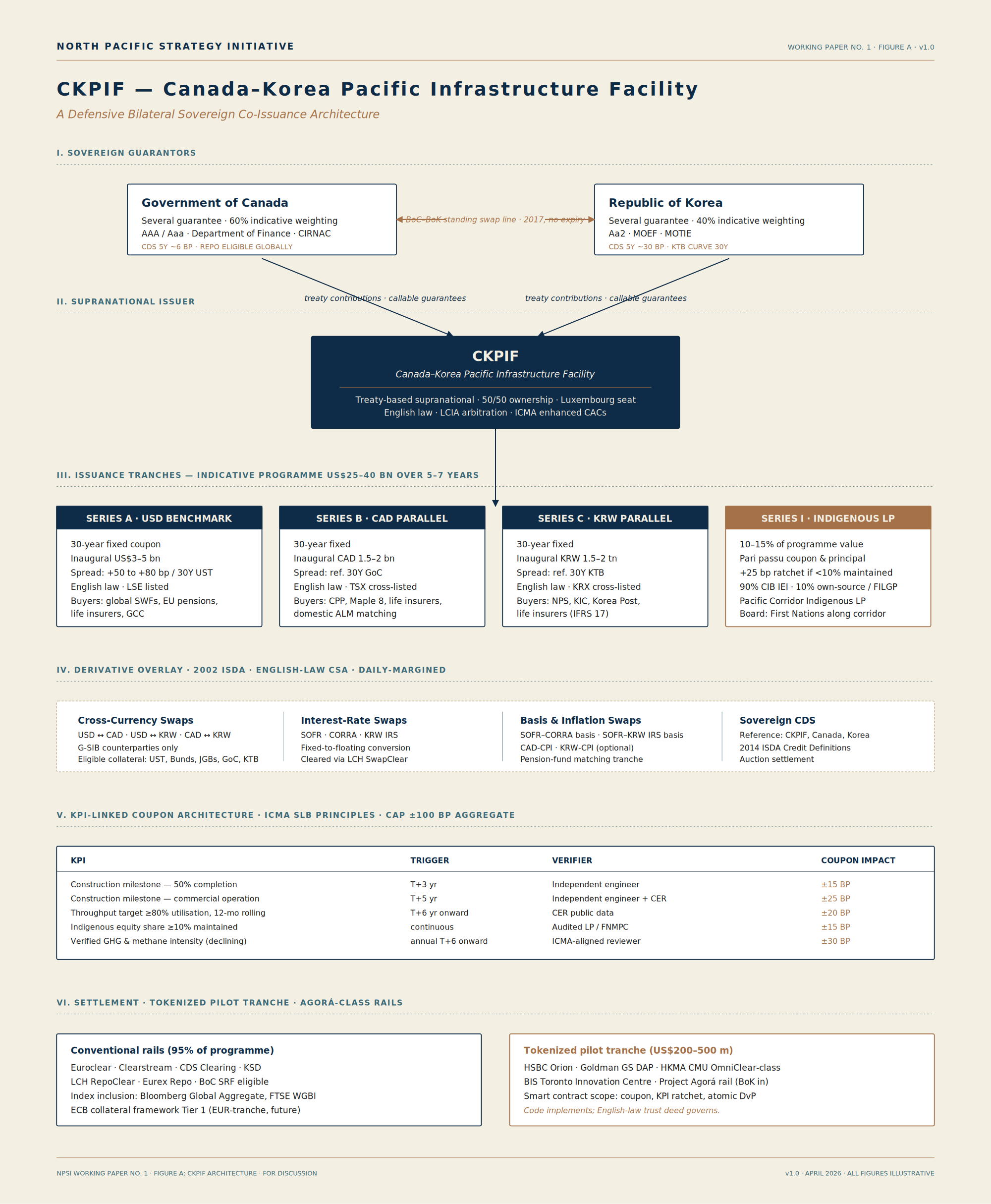

- No clean precedent exists for a bilateral co-issued sovereign bond outside supranational vehicles. The closest analogues are EU NGEU/SURE, EIB/NIB project bonds, and the Islamic Development Bank. The most realistic legal wrapper is a treaty-based supranational SPV — the Canada-Korea Pacific Infrastructure Facility (CKPIF) — seated in a neutral jurisdiction, with explicit, non-joint-and-several guarantees from each sovereign, governed by English law with submission to LCIA arbitration.

- Currency architecture should be a USD benchmark tranche with parallel CAD and KRW tranches, all swapped through ISDA-documented cross-currency overlays into the project's natural cash-flow currency. This preserves USD market depth while building parallel CAD/KRW curves usable by Korean and Canadian institutions for ALM purposes.

- The KPI-linked coupon overlay should follow ICMA Sustainability-Linked Bond Principles with conventional 25 bp step-ups for missed milestones — the dominant market structure (~60% of all SLBs use this calibration). KPIs should be construction milestones, throughput targets, Indigenous equity share maintenance, and verified GHG performance — not political conditions.

- Indigenous co-ownership must be designed in at issuance, not retrofitted. The First Nations Major Projects Coalition's track record, the CIB Indigenous Equity Initiative, the federal Indigenous Loan Guarantee Program, Coastal GasLink's 10% First Nations LP option, and the Nisga'a 50% PRGT acquisition give a robust template.

- The smart-contract layer should be modest and conservative: digital-bond issuance via the BIS Toronto Innovation Centre's payments rail and HSBC Orion / Goldman GS DAP / HKMA CMU OmniClear-class infrastructure, with smart-contract automation limited to coupon payment, KPI-trigger coupon adjustment, and post-trade reconciliation.

- A realistic placement target is a US$25–40 bn programme over 5–7 years in benchmark-sized tranches (US$3–5 bn), priced approximately +50 to +80 bp over the 30-year US Treasury at launch — comparable to EU NGEU pricing relative to Bunds and to a blend of Canada and Korea sovereign credit (Canada AAA/Aaa, Korea Aa2). This range is illustrative.

- Pipeline execution risk is the binding constraint, not financial-engineering risk. Bill C-48 still legally prohibits oil tanker traffic >12,500 t at Prince Rupert and Kitimat; the Carney–Smith MOU of 27 November 2025 commits both governments to amending the Act if necessary but Coastal First Nations and the Assembly of First Nations have publicly opposed any new oil pipeline to the north coast. The bond is buildable; the pipeline is the question. The defensible approach is to design the financial architecture so it can be deployed against an alternate north-coast project (LNG, critical minerals corridor, North Coast transmission line) if oil-to-Prince-Rupert proves politically unattainable.

Bottom line: every component of the proposed instrument exists in liquid form today. The novelty is the bilateral sovereign co-issuance and the bundling. The instrument can plausibly attract Tier-1 institutional placement without any exotic structures, on legal foundations equivalent to those used by EIB, the European Commission, NIB, IsDB, and supranational digital-bond issuers since 2018. The political and Indigenous-consent questions, not the financial engineering, are the binding constraints.

1. Sovereign Co-Issuance Precedents

The closest precedent at scale

The European Commission's NGEU and SURE programmes are the largest and most relevant precedent for jointly-backed sovereign issuance, even though they are technically supranational, not bilateral. Total EU borrowing under NGEU, SURE, MFA, and related programmes is approaching €1 trillion outstanding by end-2026, with SURE issuance alone reaching ~€100 bn between October 2020 and December 2022, and NGEU on track to ~€800 bn in current prices through 2026.

Two important features:

- No joint-and-several liability. EU member states are not jointly and severally liable for NGEU. Instead, NGEU is guaranteed by the EU budget through a temporary 0.6% headroom increase; SURE adds an additional layer of irrevocable callable guarantees from member states.

- Pricing as supranational, not as sovereign. Despite the joint backing, EU bonds trade at a discount relative to similarly-rated euro-area sovereigns (Bunds, OATs, Dutch DSLs), reflecting weaker liquidity and the absence of an associated derivatives market.

The first NGEU 10-year tranche launched in June 2021 was priced at about 32.3 bp over the equivalent Bund; the inaugural NGEU bond was the largest single-tranche syndicated transaction in capital markets history. The ECB documents that as of April 2026, EU bonds remain less liquid than core sovereigns and have not yet achieved full safe-asset status — a critical lesson for designing CKPIF.

Other supranational precedents

- European Investment Bank: ~€450 bn outstanding; treaty-based supranational; AAA across all three majors. Pioneered project bonds and tokenised bonds (Project Venus, GBP digital bond).

- Nordic Investment Bank: treaty-based, AAA, owned by 8 sovereigns; demonstrates that small/medium-power groupings can issue at AAA spreads.

- Islamic Development Bank: 57 sovereign members; sukuk and conventional both, frequently dollar-denominated, English-law.

- African Development Bank: AAA, multi-sovereign owned, regularly issues benchmark dollar bonds.

- ASEAN+3 AMRO: regional surveillance body that supports the Chiang Mai Initiative Multilateralisation (CMIM) currency-swap network — not an issuer, but a precedent for regional financial cooperation.

Bilateral sovereign co-issuance — is there a clean precedent?

No. Extensive review of sovereign debt practice finds no genuine bilateral sovereign co-issuance with two co-equal joint-and-several issuers (excluding currency unions). The standard form is one issuer with the other providing guarantees, or a supranational SPV owned by both. The proposed CKPIF would therefore be a first-of-its-kind structure, but it can be assembled entirely from off-the-shelf components: NGEU-style budget guarantee (without the headroom), EIB-style treaty supranational, ICMA Green/SLB principles, ISDA derivatives documentation, and Luxembourg-listed New York or English law bonds.

Existing Canada–Korea bilateral financial infrastructure

- Standing currency swap line, Bank of Canada – Bank of Korea, signed 15 November 2017, no expiration date and no preset limit. This is a permanent CAD-KRW liquidity backstop and is the single most important existing piece of bilateral plumbing — it removes the residual liquidity-failure tail risk that would otherwise sit on the swap overlays of a Canada–Korea bond.

- Canada–Korea Free Trade Agreement (CKFTA), in force 1 January 2015. Bilateral merchandise trade has doubled to ~C$24.5 bn in 2024; 99% of Canadian exports now have duty-free access; full implementation by 2032 will eliminate Korean tariffs on 99.75% of Canadian exports.

- Joint infrastructure financing precedent: KOGAS holds a 5% interest in LNG Canada (the largest single energy-project investment in Canadian history); POSCO is active in Canadian critical minerals; Hanwha Ocean signed a CAD$345 m MOU with Algoma Steel in late 2025 in connection with the Canadian Patrol Submarine Project.

Recommended legal wrapper for CKPIF

A treaty-based supranational, owned 50/50 by Canada and Korea, with the following stack:

- Head-office and seat: Luxembourg (EU passport for prospectus, standard for EIB/ESM-class issuers), with a Singapore subsidiary for Asian distribution.

- Governing law of bonds: English law, with London-seated LCIA arbitration; submission to the courts of England and Wales as backstop.

- Liability structure: explicit several (not joint) guarantees from Canada and Korea, in agreed proportions (e.g., 60/40 reflecting GDP weight or project beneficial-interest ratios), with a callable second-loss tranche from a budget-style headroom mechanism funded by both treasuries.

- Collective Action Clauses (CACs): standard ICMA enhanced model with single-limb aggregation across the programme.

- Listing: Luxembourg Stock Exchange primary, Singapore Exchange secondary.

2. Project Bond and Infrastructure Bond Mechanics

Construction-phase vs operations-phase tranching

A 30-year pipeline-financed bond should be tranched along the project lifecycle. Tranche A (construction phase, 5–7 years) is backed primarily by sovereign guarantees and a federal completion guarantee; coupon includes a construction-risk premium; principal secured by a project Reserve Account funded at issuance. Tranche B (operations phase, 23–25 years) is backed by availability payments and/or revenue contracts (take-or-pay shipping commitments from KOGAS, POSCO, Korean utilities and refiners, plus other Asian off-takers); coupon steps down once commercial operation date is achieved and KPIs verified.

The TMX precedent supports this model: about 80% of TMX system capacity (707.5 Mb/d of the 890 Mb/d) is now reserved for committed shippers under long-term take-or-pay contracts.

Sustainability-linked / KPI-linked structure

The sustainability-linked bond market exceeds $175 bn cumulative issuance from 230 issuers in 53 countries, following the 2019 Enel inaugural and ICMA's June 2020 SLB Principles. Standard parameters from the empirical literature: 25 bp step-up is the dominant penalty calibration (~60% of SLBs); average step-up across the market is 24.8–31.2 bp.

KPIs must be material, quantifiable, externally verifiable on a benchmarked basis, and have at least 3 years of historical data. ICMA SLB Principles allow both step-up and step-down ratchets.

Recommended KPIs for CKPIF

Each carrying ±15–25 bp coupon adjustment, capped at ±100 bp aggregate: construction milestone — 50% completion (T+3y, ±15 bp); construction milestone — commercial operation (T+5y, ±25 bp); throughput target ≥80% utilisation, 12-mo rolling (T+6y onward, ±20 bp); Indigenous equity share ≥10% maintained (continuous, ±15 bp); verified GHG intensity (annual from T+6y, ±20 bp); methane intensity (annual from T+6y, ±10 bp).

Project-finance protection stack

Standard, off-the-shelf: completion guarantees from Canada and Korea (several, callable, sized to construction-tranche outstanding); liquidated damages clauses in the EPC contract; performance bonds sized to ~10–15% of EPC value; reserve accounts (Debt Service Reserve, Maintenance Reserve, Major Maintenance Reserve); off-take contracts with KOGAS, Korean refiners (S-Oil, GS Caltex, SK Energy, Hyundai Oilbank), and one or more Indian or Japanese counterparties for diversification.

3. Derivative Overlay Architecture

A USD-benchmark issuance with parallel CAD/KRW tranches will run the following ISDA-documented overlays: cross-currency swaps (USD↔CAD, USD↔KRW); interest-rate swaps (fixed-to-floating); inflation swaps (CAD-CPI, KRW-CPI, optional); basis swaps (SOFR–CORRA, SOFR–KRW IRS basis). All overlays governed by 2002 ISDA Master Agreement with 2021 Definitions, English-law CSA, and bilateral collateral posting in cash and US Treasuries / Bunds / JGBs / CGBs as eligible collateral.

Sovereign default scenarios under ISDA

Under ISDA, a sovereign Credit Event (Failure to Pay, Repudiation/Moratorium, Restructuring) triggers Auction settlement under the 2014 ISDA Credit Derivatives Definitions. For Canada, Korea, and the supranational CKPIF, this is essentially a tail-of-tail event. Note that EU restructuring of Greek debt in 2012 was carefully structured to avoid triggering CDS, a precedent worth being aware of, but not an obstacle to CKPIF design.

Sovereign CDS — Canada and Korea, 2026

- Canada 5-year CDS: trades at very tight levels, typically in single-digit bp; ranks among the lowest-risk sovereigns globally.

- Korea 5-year CDS: typically 25–45 bp range historically, reflecting Aa2 rating and Korean peninsula geopolitical risk premium.

- CKPIF's implied CDS would price between these — meaningfully wider than Canada-only, narrower than Korea-only, with a small "novelty premium" that should compress over the first 2–3 years of issuance.

Repo market acceptance

Both Canadian Government Bonds and Korean Treasury Bonds (KTBs) are accepted as collateral in major repo and securities-lending markets. The CKPIF should target inclusion in: LCH RepoClear, Eurex Repo, BoC Standing Repo Facility eligible securities, Bank of Korea repo market, and the ECB collateral framework Tier 1 (achievable for AAA/Aaa supranationals with EUR-denominated tranches). Repo-eligibility is essential; without it, large bank Treasuries, dealers, and pension funds cannot use the bond efficiently for ALM, materially reducing demand.

4. Currency Architecture

The recommended structure is a USD benchmark plus parallel CAD and KRW tranches, all swapped. This combines USD market depth with native-currency exposure for institutions, allows parallel curves to be built, and preserves the diversification narrative without taking on the operational complexity and investor-education burden of a basket-denominated structure.

The 2026 de-dollarisation landscape — sober assessment

The empirical record since 2022 is mixed, and any briefing must avoid over-claiming. Dollar share of official FX reserves has declined only modestly, broadly consistent with the pre-2022 trend of ~0.5 percentage points per year. Goldberg/Hannaoui (2024) and Chinn et al (2024) find no significant additional dollar decline attributable to financial sanctions. Gold has gained share as a sanction-proof reserve asset. CIPS (China's cross-border payments system) has grown but remains under 5% of SWIFT throughput. Russia–China bilateral trade is now ~90% settled in RMB or RUB. Project mBridge (BIS, PBoC, HKMA, BoT, CBUAE) is a live multi-CBDC platform but BIS withdrew operational involvement in 2024. Project Agorá includes the Bank of Korea but not yet the Bank of Canada — though the BIS Toronto Innovation Centre is active.

Implication. CKPIF's de-dollarisation pitch is real but should be framed conservatively — as adding optionality and building a parallel rail, not as displacing the dollar. The dollar will remain dominant through the 30-year life of the bond. The KRW's increasing role in bilateral trade settlement is the natural locus of KRW-tranche placement.

5. Tokenized Sovereign Bonds and Smart Contract Layer

The BIS Toronto Innovation Centre, opened June 2024 with Bank of Canada, focuses on next-generation FMI, suptech, and open finance, with active projects including Mandala (smart-contract AML/CFT compliance) and FuSSE (fully scalable settlement engine). Toronto and Seoul are therefore both first-rank participants in the tokenisation experiment, which is rare and strategically useful.

Tokenised government-bond pilots

By 2025, tokenised SSA bonds have moved past the experimental phase into routine issuance at HK$10 bn-sized transactions. Notable pilots: World Bank Bond-i (2018, A$110 m, Ethereum private), EIB digital bond #1 (2021, €100 m, public Ethereum + onChain), HKMA Project Genesis green bond (2021), HKMA tokenised green bond (2023, HK$800 m, Goldman GS DAP), EIB Project Venus (2022, €100 m), HKSAR digital green bonds (2024, HK$6 bn equivalent across HKD/RMB/USD/EUR), HKSAR third tokenised series (2025 Q4, HK$10 bn, CMU OmniClear). Cumulative SSA tokenised by end-2024: ~US$1.6 bn.

What can smart contracts realistically automate?

Conservative scope appropriate for CKPIF: coupon payment (date-triggered); KPI-triggered coupon adjustment (oracle-fed, for objective externally-verified KPIs only); atomic DvP settlement in primary issuance and secondary trading; maturity redemption.

What cannot and should not be automated: material principal-affecting events (default, restructuring, CAC vote); sovereign-level political triggers (sanctions, force majeure, trade-disruption events); smart contracts that purport to override contractual force-majeure or "act of state" defences.

Legal enforceability

Under both English and New York law, smart-contract clauses are enforceable to the extent they form part of a binding written contract. The 2019 UK Jurisdiction Taskforce Statement (chaired by Sir Geoffrey Vos) confirmed cryptoassets and smart contracts can be property and binding contracts under English law. New York Uniform Commercial Code Article 12 (effective 2023) provides a parallel framework. The HKMA and EIB issuances have all been issued under English law with smart-contract layers; the precedent is solid. Key drafting principle: the smart-contract code should implement (not replace) the underlying English-law trust deed, with a "code-vs-prose" precedence clause favouring the prose master document.

6. Safe Asset Substitution and Flight-to-Quality

The seminal Caballero / Farhi / Gourinchas literature defines a safe asset as a debt instrument that preserves its value during adverse systemic events, and documents a chronic global safe-asset shortage. This literature provides direct intellectual cover for CKPIF: a Canada–Korea co-issued AAA-quality bond would expand global safe-asset supply — a recognised public good — and would not be vulnerable to the "fiscal exhaustion" risk that constrains pure US Treasury issuance.

Where would CKPIF sit?

A reasonable hierarchy of 30-year benchmark spreads over the 30-year US Treasury at issuance: Bunds (DE) typically –20 to +20 bp; Swiss Confederation –50 to –20 bp; Singapore Government Securities +20 to +40 bp; EU NGEU +40 to +60 bp; EIB +30 to +50 bp; Australian Commonwealth +40 to +70 bp; Canada Government 30-year +30 to +60 bp; Korea Treasury Bond 30-year +60 to +110 bp. CKPIF (estimated, indicative): +50 to +80 bp.

The +50–80 bp range reflects a blend of Canada and Korea sovereign credit, a modest novelty/illiquidity premium for the first 2–3 years of issuance, and the supranational discount documented for NGEU. As a 30-year curve develops and benchmark issuance reaches US$15–25 bn, this spread should compress to the +30–60 bp range. All numbers are illustrative; actual pricing depends on programme structure and market conditions at launch.

7. Stress Scenario Analysis

US sovereign downgrade or technical default

Capital flow: gold ↑, Bunds ↑, JGBs ↑, Swiss ↑, AAA-non-US sovereigns ↑. CKPIF behaviour: spread vs UST narrows; absolute price rises modestly; KRW tranche outperforms USD tranche. Net beneficiary scenario.

Aggressive USD weaponisation extended to Canadian or Korean entities

The existential threat the instrument is designed against. The 2022 freezing of ~half of Russia's ~$640 bn FX reserves (~$300 bn) is the relevant precedent. CKPIF behaviour: USD tranche may face settlement frictions if directly affected; CAD and KRW tranches insulated. The instrument's bilateral, multi-tranche design is the hedge. Note this scenario is highly tail-risk for a Canada–Korea pairing; both are US treaty allies.

Major tariff shock against Canadian exports

2025–26 has shown this is no longer hypothetical. CKPIF behaviour: bond performs well; the thesis is validated; demand for diversification accelerates. Pipeline project's economic case strengthens.

Korean peninsula military event

Korea CDS spreads typically widen 50–150 bp on serious provocations. CKPIF behaviour: KRW tranche underperforms; USD and CAD tranches relatively unaffected; the several-not-joint guarantee structure means Canada's portion is unimpaired. Net effect: a 30–60 bp temporary spread widening, manageable.

Middle East oil shock

The February 2026 Strait of Hormuz crisis is described by the IEA as the largest oil supply disruption in history, with ~20% of world seaborne oil and ~20% of LNG normally transiting Hormuz disrupted. Korea imports 95% of its crude through the Strait. This scenario is the live tailwind. Korean energy security is the most immediate buyer-side rationale for CKPIF.

China financial stress / Taiwan contingency

Capital flow: violent rotation into AAA-non-China-exposed safe assets. CKPIF behaviour: AAA-Pacific positioning is the natural beneficiary. Likely tightening of CKPIF spreads vs Korean sovereign curves; widening vs Canadian.

Global recession / dash-for-cash

2020 showed even UST initially sold off in the dash-for-cash; central bank liquidity was the binding constraint. CKPIF behaviour: short-term dislocation; spread widens 50–100 bp; resolves once central bank liquidity provided. The BoC–BoK standing swap line is the structural mitigant.

8. Fort McMurray to Prince Rupert — Real Political Landscape

Current west-coast bitumen export state

Trans Mountain Expansion (TMX) has been in commercial service since May 2024; tripled system capacity from 300 Mb/d to 890 Mb/d. Average utilisation has been 82–88% since startup. 12 months post-TMX, BC crude oil export volumes increased more than 6× year over year; non-US destinations took 48.1% (China 31.9%, Hong Kong 7.1%, Singapore 6.3%, South Korea 1.6%, India 1.2%).

Northern Gateway autopsy — why it died

Federal cabinet approved June 2014 (Harper) with 209 conditions. Federal Court of Appeal Gitxaala Nation (2016) quashed approval over Phase IV consultation duty. Trudeau cabinet rescinded approval November 2016 and tabled Bill C-48. Critical lesson: had ~30 of 42 bands along the route signed equity agreements with Enbridge for a 10% equity stake; nonetheless the project's coastal terminus and the absence of First Nations economic leadership (vs minority equity participation) were politically fatal.

Bill C-48 — the binding legal constraint

The Oil Tanker Moratorium Act, in force May 2019, prohibits oil tankers carrying >12,500 tonnes of crude or persistent oil from loading or unloading at ports between the northern tip of Vancouver Island and the Alaska border. Both Prince Rupert and Kitimat are within the moratorium zone. Two paths to enable a pipeline: full repeal (politically heavy lift, opposed by Coastal First Nations and BC government); or public-interest exemption / designation under the Building Canada Act 2025. The Carney–Smith MOU of 27 November 2025 commits to amending the Act "if necessary."

Federal, BC, and First Nations positions (April 2026)

- Federal (Carney): pro-pipeline conditional on private-sector proponent, Indigenous co-ownership, "national interest" designation; Building Canada Act and Major Projects Office in place.

- Alberta (Smith): actively lobbying; will submit project application to Major Projects Office by July 2026.

- British Columbia (Eby): publicly opposed; signed the Coastal First Nations North Coast Protection Declaration on 5 November 2025.

- Coastal First Nations: opposed; staunch maintenance of tanker ban.

- Assembly of First Nations: passed unanimous emergency resolution 2 December 2025 demanding withdrawal of MOU.

- Some Indigenous voices supportive: Dale Swampy (National Coalition of Chiefs), Indigenous Resource Network, Athabasca Indigenous Investments, First Nations LNG Alliance.

Economics — value at stake

WCS-WTI differential is structurally $11–15/bbl in normal times. Post-TMX, the differential narrowed by ~$3/bbl, generating ~$4 bn of additional industry revenue. Every $1/bbl swing in differential equals ~$740 m in Alberta budget revenue. A 1 Mb/d Fort McMurray–Prince Rupert pipeline at $5/bbl avoided discount and 365-day operation generates ~$1.8 bn/yr in additional economic rent; over a 25-year operational tenor, that is ~$45 bn nominal — sufficient to service a $25–35 bn bond programme.

9. Indigenous Equity Architecture

The institutional landscape

The First Nations Major Projects Coalition (FNMPC) has 186 member nations advising on 21 projects worth ~$45 bn. The Canada Infrastructure Bank Indigenous Equity Initiative (IEI) provides loans of $5–100 m at minimum Government of Canada rates, repayment up to 15 years, financing up to 90% of Indigenous equity stake. The federal Indigenous Loan Guarantee Program ($5 bn announced in Budget 2024) provides sector-agnostic backing.

Live precedents

- Coastal GasLink (TC Energy/KKR/AIMCo): 10% LP option, two LPs representing 16 of 20 Nations.

- Athabasca Indigenous Investments: 11.57% NOI in 7 Enbridge pipelines; $1.12 bn purchase.

- PRGT (Nisga'a Nation + Western LNG): 50% Nisga'a ownership; full transfer from TC Energy in 2024.

- North Coast transmission: ~50% First Nations equity in development through BC Indigenous Power Coalition.

Designed-in Indigenous tranche for CKPIF

A separate Series I (Indigenous) tranche, sized at 10–15% of total programme value:

- Indigenous Limited Partnership ("Pacific Corridor Indigenous LP") holds the Series I tranche, governed by a board with proportional First Nations representation along the corridor.

- Series I subscription financed 90% by CIB IEI direct loans, 10% by First Nations own-source revenue / treaty trust funds / federal Indigenous Loan Guarantee Program co-funding.

- Series I economic rights: pari passu coupon and principal with Series A and B; step-up coupon adjustment of +25 bp if Indigenous equity share falls below 10% — a structural protection ratchet.

- Governance rights: Nation-level consent on route changes through traditional territories; veto right on amendments to Indigenous-equity KPIs; director representation on CKPIF supranational board.

- Cost of capital: CIB IEI rate is significantly below CKPIF coupon — generating positive carry spread for the Indigenous LP, monetisable as own-source revenue.

This structure makes Indigenous co-ownership financially attractive, politically durable, and executable — every component already exists.

10. Korean Counterparty Landscape

Institutional buyers

National Pension Service (NPS, ~$900–960 bn) is the anchor buyer; could place $3–5 bn. Korea Investment Corporation (KIC, $206.5 bn) targets $1–2 bn. Korea Post / Korea Teachers' Pension (combined ~$200 bn) targets $1–2 bn combined. Korean life insurers (Samsung Life, Hanwha Life, Kyobo, ~$700 bn combined) have IFRS 17-driven 30-year duration matching demand and could place $2–3 bn combined. The BoK–BoC standing swap line gives the KRW tranche a credible liquidity backstop.

Korean strategic investment in Canada to date

- KOGAS 5% in LNG Canada (largest single-energy-project investment in Canadian history, FID 2018).

- Hanwha Ocean – Algoma Steel: USD 250 m / CAD 345 m structural arrangement linked to CPSP.

- POSCO active in Canadian critical minerals (lithium, nickel) and steel.

- Hyundai Motor Group / LG Energy Solution: EV supply chain investments in Ontario.

- Korea Zinc, EcoPro, LIG Nex1: critical minerals and defence active in Canada.

The HBM strategic bundle

Samsung and SK Hynix together produce ~90% of global HBM (high-bandwidth memory) used in AI processors; HBM4 mass production launched February 2026 with NVIDIA's Rubin platform. HBM has become "a strategic asset comparable to energy resources or critical minerals." Korean dependence on Canadian critical minerals — copper, nickel, cobalt, lithium, rare earths — for the HBM/AI/EV stack is the natural strategic bundle. Pacific Energy Corridor and a parallel Critical Minerals Corridor can be packaged as a single CKPIF programme with two separate use-of-proceeds tranches.

11. Political Feasibility and Champions

Ottawa champions (April 2026)

Prime Minister Mark Carney (Liberal, sworn in March 2025): former Bank of Canada and Bank of England governor, deep capital-markets fluency. Minister of Energy and Natural Resources Tim Hodgson: former Goldman Sachs Canada CEO and Bank of Canada special advisor. Major Projects Office: established 2025, mandate to bring projects to FID within two years.

Seoul champions (April 2026)

President Lee Jae-myung (Democratic Party, inaugurated 4 June 2025): explicit policy alignment with Canada on critical minerals, clean energy, defence cooperation. Ministry of Trade, Industry and Energy (MOTIE) — Minister Kim Jung-kwan: lead on industrial policy and energy security. Bank of Korea (Governor Rhee Chang-yong): operating partner via the standing swap line and Project Agorá.

American reaction pathway and how to harden the instrument

Hardening measures: several, not joint, guarantees; English-law governance, Luxembourg domicile, Singapore/Tokyo secondary listing; bookrunner consortium balanced across geographies; no use of US Treasury-managed clearing for KRW or CAD tranches; smart-contract layer on jurisdictionally-distributed DLT explicitly not on a US-jurisdiction primary node; framing externally as defensive counterparty-risk diversification, never anti-American.

Sequencing — first three concrete steps

Step 1 (months 0–6). Track-1.5 dialogue and feasibility paper. Convene CIRI / APF Canada / KIEP / NPS Investment Management / Bank of Canada / Bank of Korea senior advisors on a "Pacific Infrastructure Co-Issuance Facility" feasibility paper. Soft-sound NPS, KIC, Korea Post, CPP, OTPP, Maple 8 on indicative interest.

Step 2 (months 6–12). Treaty negotiation and project selection. Bilateral treaty drafting (Global Affairs Canada / MOFA Korea), modelled on the EIB treaty. Project shortlist including but not limited to the pipeline. FNMPC engagement on Indigenous tranche design from day one.

Step 3 (months 12–18). Inaugural issuance. Inaugural USD benchmark of $3–5 bn (even before any pipeline FID), use-of-proceeds tied to a non-controversial first project. Subsequent CAD and KRW tranches at $1–2 bn each within 6 months. Indigenous Series I issued in parallel. Tokenised pilot tranche (~$200–500 m).

12. Risks and Failure Modes

Political reversal in Canada or Korea

Canada: a future Conservative government would likely be more pipeline-friendly but might have less appetite for a Korea-paired structure. The instrument should be designed as sovereign-of-Canada legal commitment, with binding treaty obligations that cannot be unilaterally revoked. Korea: 5-year presidential cycle means policy shifts. Treaty entrenchment is the only true protection.

Counterparty risk in derivatives

30-year cross-currency swaps create long-dated counterparty exposure. Mitigation: mandatory CSA collateralisation with daily margining, central clearing via LCH SwapClear where available, bilateral arrangements with G-SIBs only.

Secondary market liquidity risk

The first 2–3 years of issuance will see wider bid-ask spreads (NGEU lesson). Mitigation: market-maker commitments from the underwriting syndicate; tap issuance schedule pre-announced; inclusion in major bond indices once outstanding volume reaches threshold.

Risk of being seen as politically provocative

Mitigation: framing discipline. Never position as anti-American or anti-dollar; always as a Pacific safe-asset additive, supplementing not replacing global financial architecture. Keep US bookrunners welcomed in the syndicate.

Pipeline execution risk — the binding constraint

This is the highest-probability failure mode. Mitigation: decouple financial architecture from pipeline binary. The CKPIF facility should be designed to fund any qualifying Pacific corridor infrastructure, of which the pipeline is one possible use. If the pipeline fails regulatory or consent processes, the facility funds the North Coast transmission line, Cedar LNG follow-on, Ksi Lisims LNG, critical minerals corridor, or other qualifying projects. Front-load Indigenous co-ownership and consent processes before any construction commitment. Stage the pipeline as Phase 2 of CKPIF.

13. Concluding Synthesis

The proposed Canada–Korea co-issued sovereign infrastructure bond is technically feasible using only conventional, internationally-accepted financial instruments. Every component — supranational treaty issuance (EIB/EU), KPI-linked coupons (ICMA SLB, ~$175 bn market), ISDA cross-currency overlays, BoC–BoK standing swap, ICMA enhanced CACs, CIB Indigenous Equity Initiative loans, CGL/PRGT-style Indigenous LP equity, HSBC Orion / GS DAP tokenised settlement, Project Agorá payments rail — exists in liquid, regulated, well-precedented form in 2026.

The novelty is the combination and the bilateral co-issuance, for which there is no clean precedent. The instrument should be framed and placed as a Pacific safe-asset additive, sized initially at $25–40 bn over 5–7 years, priced approximately +50–80 bp over 30-year UST at launch, with tightening to +30–60 bp as the curve develops.

The strategic value is real but should be claimed with discipline: the instrument provides Canada with counterparty-risk diversification, parallel financial-rail optionality, and a credible mechanism for Indigenous economic reconciliation embedded in nation-building infrastructure. It does not displace the dollar; it does not break with the United States; it does not hedge Canadian sovereignty against a hypothetical US adversary. It builds an additional, AAA-quality, treaty-backed, Pacific-anchored bid-side liquid asset for global institutional money.

The binding constraint is not financial engineering. It is Indigenous consent for a north-coast oil pipeline, and the consequent legal status of Bill C-48. The defensible architecture is therefore to build the financial facility independent of the pipeline's binary outcome, and to permit it to fund any qualifying Pacific corridor infrastructure, with the pipeline as the headline candidate but not the sole use-of-proceeds.

If the pipeline ultimately proceeds, CKPIF is the natural and most efficient funding vehicle. If it does not, CKPIF still delivers the defensive financial architecture — and that is what Canadian middle-power sovereignty actually requires.

Engage with this Working Paper

Substantive comment, technical critique, and named response are welcomed. The Working Paper is maintained as a public version-controlled document on GitHub; the version above is the editorially-controlled v1.0.